We Spent Years Inside Singapore's Banking System.

These Are the 5 Property Mistakes We Saw Destroy the Most Wealth.

We Spent Years Inside Singapore's Banking System. These Are the 5 Property Mistakes We Saw Destroy the Most Wealth.

What an ex-investment banker and ex-mortgage broker tell their clients to do instead.

What an ex-investment banker and ex-mortgage broker tell their clients to do instead.

We Spent Years Inside Singapore's Banking System. These Are the 5 Property Mistakes We Saw Destroy the Most Wealth.

We Spent Years Inside Singapore's Banking System. These Are the 5 Property Mistakes We Saw Destroy the Most Wealth.

What an ex-investment banker and ex-mortgage broker tell their clients to do instead.

What an ex-investment banker and ex-mortgage broker tell their clients to do instead.

Most property decisions in Singapore are made on incomplete information

In 2019, Avenue South Residences sold over 90% of its units on launch day.

Florence Residences launched the same year and sold under 30%.

Today, Florence Residences has appreciated 25.9%.

Avenue South Residences, 10.8%.

Two developments. Same year. Opposite launch results.

And the one that looked like the obvious winner ended up being the weaker investment.

If that surprises you, you are not alone.

It surprised us too when we first entered real estate from investment banking and mortgage advisory.

And it pointed to something we have seen over and over since:

Most property decisions in Singapore are made with a significant blind spot that the standard buying process is simply not designed to catch.

If you are an HDB owner thinking about upgrading, you have probably felt the edges of this blind spot already, even if you could not name it.

You have done your homework.

Scrolled PropertyGuru after the kids fall asleep.

Checked your estimated loan using online calculators.

Asked friends who recently upgraded how they did it.

Maybe visited a showflat or two.

And yet something still does not feel settled.

You are not sure if the market is too high right now, or if waiting will only make things worse.

You are not sure how to tell a genuinely sound purchase from one that just looks good on the surface.

And at some point, you have probably thought:

"I just want to make sure I don't get this wrong."

"I just want to make sure I don't get this wrong."

That feeling is the right instinct.

Because this is not a decision where you get a second chance if something goes sideways.

For most families, this is the single largest financial commitment they will ever make.

Larger than their CPF. Larger than their savings. The kind of decision that shapes the next 10 to 15 years of your family's financial life.

And yet, most people make this decision with a significant

blind spot they do not even know they have.

The Uncomfortable Truth About Your Upcoming Upgrade

The Uncomfortable Truth About Your Upcoming Upgrade

If you are an HDB owner thinking about upgrading, you have probably spent more time on this decision than you would like to admit.

If you are an HDB owner thinking about upgrading, you have probably spent more time on this decision than you would like to admit.

Scrolling PropertyGuru after the kids fall asleep.

Running mental calculations on whether the finances work.

Asking friends who recently upgraded how they did it.

Wondering if the market is too high right now, or if waiting will only make things worse.

Scrolling PropertyGuru after the kids fall asleep.

Running mental calculations on whether the finances work.

Asking friends who recently upgraded how they did it.

Wondering if the market is too high right now, or if waiting will only make things worse.

And at some point, you have probably thought:

"I just want to make sure I don't get this wrong."

"I just want to make sure I don't get this wrong."

That feeling is the right instinct.

Because this is not a decision where you get a second chance if something goes sideways.

For most families, this is the single largest financial commitment they will ever make.

Larger than their CPF. Larger than their savings. The kind of decision that shapes the next 10 to 15 years of your family's financial life.

And yet, most people make this decision with a significant

blind spot they do not even know they have.

We came from an industry where buying a "good deal" purely on its profitability potential would get you fired.

We came from an industry where buying a "good deal" purely on its profitability potential would get you fired.

In investment banking, no deal gets approved based on one dimension alone.

Before any capital is committed, every transaction goes through full due diligence.

That level of rigour is standard in banking.

It is not standard in property.

That level of rigour is standard in banking.

It is not standard in property.

When we entered real estate, we expected families to have access to the same depth of analysis for the biggest purchase of their lives.

What we found was that most property decisions are made almost entirely on one dimension: the property itself.

Is the location good? Is the price reasonable? Does it have upside?

Those are important questions. But they are not the only questions.

And when they are the only questions being asked, families end up making million-dollar commitments on a fraction of the information they actually need.

We came from an industry where buying a "good deal" purely on its profitability potential would get you fired.

We came from an industry where buying a "good deal" purely on its profitability potential would get you fired.

In investment banking, no deal gets approved based on one dimension alone.

Before any capital is committed, every transaction goes through full due diligence.

That level of rigour is standard in banking.

It is not standard in property.

That level of rigour is standard in banking.

It is not standard in property.

When we entered real estate, we expected families to have access to the same depth of analysis for the biggest purchase of their lives.

What we found was that most property decisions are made almost entirely on one dimension: the property itself.

Is the location good? Is the price reasonable? Does it have upside?

Those are important questions. But they are not the only questions.

And when they are the only questions being asked, families end up making million-dollar commitments on a fraction of the information they actually need.

The Three Dimensions Behind Every Property Decision That Actually Works

In our experience, every sound property decision requires three dimensions of analysis. Not one.

The first dimension

THE FIRST DIMENSION

Which property to buy.

This is what most of the conversation revolves around.

And even here, we have found that the standard analysis is far more surface-level than most buyers realise.

Most property evaluations focus on location, price, and developer reputation. Those are starting points, not conclusions.

In investment banking, we would never approve a deal based on those factors alone.

We would ask:

👉 How many transactions has this development recorded in the past 12 months?

👉 What does the buyer pool actually look like, and is it growing or contracting?

👉 If comparable units in the area are selling faster and at higher prices, what is creating that gap?

👉 What is the realistic exit price under current market conditions, not the optimistic one?

These are not complicated questions.

But they require a habit of looking past the surface, one that institutional training drills into you over years.

We see no reason a family committing a million dollars to a single property should get less rigour than a fund committing a million dollars to a deal.

We evaluate every property using what we call our 7-Point Institutional Property Scorecard.

The same criteria we would have applied to an institutional acquisition, adapted for residential property.

Not because we are trying to be different for the sake of it. But because the standard checklist simply misses too much.

THE SECOND DIMENSION

How you pay for it.

Not just "can I afford the monthly payment?" but whether the financing structure actually protects you.

Which loan package has costs buried in the fine print. Whether your eligibility is calculated the way you think it is.

Whether there are options available to you that nobody has mentioned, because they require mortgage-level expertise to even know they exist.

Most buyers are never told about deviated rates that banks offer but do not publish.

Or about free conversion clauses within lock-in periods that can save thousands per year.

Or about the difference between a 0.75% and 1.5% cancellation penalty clause, and why it matters when you need to refinance.

These details sit in the second dimension. And they are almost always left out of the conversation.

THE THIRD DIMENSION

What happens if life does not go

according to plan.

Interest rates shift.

Cooling measures tighten.

The economy slows down.

Someone in the family loses their income.

You need to sell earlier than expected.

These are not worst-case fantasies. They are scenarios that play out for Singapore families every single year.

A sound property decision holds up across these scenarios. Not just under perfect conditions.

Most property decisions cover the first dimension at a surface level.

Almost none of them cover the second and third.

That gap is where we have seen the most wealth destroyed.

Not from buying "bad" properties, but from making decisions on an incomplete picture.

The Three Dimensions Behind Every Property Decision That Actually Works

In our experience, every sound property decision requires three dimensions of analysis. Not one.

THE FIRST DIMENSION

Which property to buy.

This is what most of the conversation revolves around.

And even here, we have found that the standard analysis is far more surface-level than most buyers realise.

Most property evaluations focus on location, price, and developer reputation. Those are starting points, not conclusions.

In investment banking, we would never approve a deal based on those factors alone.

We would ask:

👉 How many transactions has this development recorded in the past 12 months?

👉 What does the buyer pool actually look like, and is it growing or contracting?

👉 If comparable units in the area are selling faster and at higher prices, what is creating that gap?

👉 What is the realistic exit price under current market conditions, not the optimistic one?

These are not complicated questions.

But they require a habit of looking past the surface, one that institutional training drills into you over years.

We see no reason a family committing a million dollars to a single property should get less rigour than a fund committing a million dollars to a deal.

We evaluate every property using what we call our 7-Point Institutional Property Scorecard.

The same criteria we would have applied to an institutional acquisition, adapted for residential property.

Not because we are trying to be different for the sake of it.

But because the standard checklist simply misses too much.

THE SECOND DIMENSION

How you pay for it.

Not just "can I afford the monthly payment?" but whether the financing structure actually protects you.

👉 Which loan package has costs buried in the fine print.

👉 Whether your eligibility is calculated the way you think it is.

👉 Whether there are options available to you that nobody has mentioned, because they require mortgage-level expertise to even know they exist.

Most buyers are never told about deviated rates that banks offer but do not publish.

👉 Or about free conversion clauses within lock-in periods that can save thousands per year.

👉 Or about the difference between a 0.75% and 1.5% cancellation penalty clause, and why it matters when you need to refinance.

These details sit in the second dimension. And they are almost always left out of the conversation.

THE THIRD DIMENSION

What happens if life does not go according to plan.

Interest rates shift.

Cooling measures tighten.

The economy slows down.

Someone in the family loses their income.

You need to sell earlier than expected.

These are not worst-case fantasies. They are scenarios that play out for Singapore families every single year.

A sound property decision holds up across these scenarios. Not just under perfect conditions.

Most property decisions cover the first dimension at a surface level.

Almost none of them cover the second and third.

That gap is where we have seen the most wealth destroyed.

Not from buying "bad" properties, but from making decisions on an incomplete picture.

This is why our backgrounds matter.

Julynn spent years in investment banking, working with Real Estate Investment Trusts across retail, industrial, and office sectors.

Her job was to stress-test deals for a living.

Model the downside.

Challenge every assumption.

Figure out what breaks before any capital moves.

She applies that same rigour to the first and third dimensions. Which property actually holds up when you look past the surface, and what happens when conditions change.

Kalcee spent three years as a mortgage broker at one of Singapore's established advisory firms.

She did not just compare interest rates. She structured financing for complex cases.

Identified hidden clauses that could cost borrowers tens of thousands.

Negotiated deviated rates with banks that are never published online.

Structured financing for cases others said could not be done.

She covers the second dimension.

How the financing is structured, what protections exist that most buyers never hear about, and where the hidden costs live.

Together, we cover what most property decisions leave out.

This is why our backgrounds matter.

Julynn spent years in investment banking, working with Real Estate Investment Trusts across retail, industrial, and office sectors.

Her job was to stress-test deals for a living.

Model the downside.

Challenge every assumption.

Figure out what breaks before any capital moves.

She applies that same rigour to the first and third dimensions. Which property actually holds up when you look past the surface, and what happens when conditions change.

Kalcee spent three years as a mortgage broker at one of Singapore's established advisory firms.

She did not just compare interest rates. She structured financing for complex cases.

Identified hidden clauses that could cost borrowers tens of thousands.

Negotiated deviated rates with banks that are never published online.

Structured financing for cases others said could not be done.

She covers the second dimension.

How the financing is structured, what protections exist that most buyers never hear about, and where the hidden costs live.

Together, we cover what most property decisions leave out.

Here is what it looks like when the second and third dimensions are missing.

In 2019, four family members pooled their resources to buy a 1-bedroom unit at One Pearl Bank.

$1.184 million.

The plan was simple: hold for three years, sell at a profit, split the gains.

DIMENSION 1: THE PROPERTY ✓

Everything checked out.

Prime District 3 location.

Walking distance to Outram Park MRT. Award-winning architecture.

A development with genuine prestige.

One Pearl Bank Condominium

The property analysis was solid. But that was the only

analysis anyone did.

DIMENSION 2: NOT CHECKED ✗

Nobody evaluated the financing implications of four co-owners on a single investment unit.

DIMENSION 3: NOT CHECKED ✗

Nobody evaluated the financing implications of four co-owners on a single investment unit.

Nobody stress-tested what would happen if the government tightened cooling measures during the holding period.

Between 2021 and 2023, ABSD for foreigners went from 20% to 60%. For Permanent Residents buying a second property, it rose from 15% to 30%.

The buyer pool for a 1-bedroom investment unit in the city centre shrank dramatically.

The exact group of buyers this family would need at exit was disappearing.

That is the third dimension. And nobody had checked it.

After three years, they sold for $1.188 million. A $4,000 "gain" on paper.

-$80,000

Real loss after stamp duty, legal fees, interest, and commissions

Four family members. Three years of tied-up capital. A property that checked every conventional box. The property was not the problem. The decision was made on one-third of the information.

During the same period, a similarly-priced 2-bedroom unit at Florence Residences that they had considered would have returned over $200,000 in profit.

Here is what it looks like when the second and third dimensions are missing.

In 2019, four family members pooled their resources to buy a 1-bedroom unit at One Pearl Bank.

$1.184 million.

The plan was simple: hold for three years, sell at a profit, split the gains.

DIMENSION 1: THE PROPERTY ✓

Everything checked out.

Prime District 3 location.

Walking distance to Outram Park MRT. Award-winning architecture.

A development with genuine prestige.

One Pearl Bank Condominium

The property analysis was solid. But that was the only

analysis anyone did.

DIMENSION 2: NOT CHECKED ✗

Nobody evaluated the financing implications of four co-owners on a single investment unit.

DIMENSION 3: NOT CHECKED ✗

Nobody evaluated the financing implications of four co-owners on a single investment unit.

Nobody stress-tested what would happen if the government tightened cooling measures during the holding period.

Between 2021 and 2023, ABSD for foreigners went from 20% to 60%. For Permanent Residents buying a second property, it rose from 15% to 30%.

The buyer pool for a 1-bedroom investment unit in the city centre shrank dramatically.

The exact group of buyers this family would need at exit was disappearing.

That is the third dimension. And nobody had checked it.

After three years, they sold for $1.188 million. A $4,000 "gain" on paper.

-$80,000

Real loss after stamp duty, legal fees, interest, and commissions

Four family members. Three years of tied-up capital. A property that checked every conventional box. The property was not the problem. The decision was made on one-third of the information.

During the same period, a similarly-priced 2-bedroom unit at Florence Residences that they had considered would have returned over $200,000 in profit.

Here is what it looks like when all three dimensions are part of the conversation.

A young couple came to us ready to upgrade. They had done their homework.

Budget of $2 million. They wanted a freehold condominium near the city.

Older boutique developments from the 1980s caught their eye.

Spacious layouts, central locations, the kind of units their parents might call "real property."

We understood the appeal.

And we could have collected a comfortable commission by helping them buy exactly what they wanted.

Instead, we asked them to let us run the full picture.

Not just "can I afford the monthly payment?" but whether the financing structure actually protects you.

Which loan package has costs buried in the fine print.

Whether your eligibility is calculated the way you think it is.

Whether there are options available to you that nobody has mentioned, because they require mortgage-level expertise to even know they exist.

Most buyers are never told about deviated rates that banks offer but do not publish.

Or about free conversion clauses within lock-in periods that can save thousands per year.

Or about the difference between a 0.75% and 1.5% cancellation penalty clause, and why it matters when you need to refinance.

These details sit in the second dimension. And they are almost always left out of the conversation.

DIMENSION 1: THE PROPERTY ✓

The older freehold condos had issues hiding behind the attractive price tags.

Ageing infrastructure that would need replacement within years.

One comparable development had recently charged residents $300 per month over two years just for lift upgrades.

Boon Keng HDB estate.

After factoring in $80,000 to $100,000 in realistic renovation costs, the "affordable" entry price was not affordable at all.

And when we checked transaction volume, the picture worsened.

Some of these boutique freehold developments had recorded just one or two transactions in an entire year.

When you can count the number of buyers on one hand, you are looking at a serious liquidity problem at exit.

DIMENSION 2: FINANCING ✓

Stretching to $2 million would have tightened their monthly cashflow significantly.

The financing stress-test showed limited buffer if interest rates moved even slightly.

DIMENSION 3: STRESS-TESTING ✓

CBD condos were facing a shrinking buyer pool.

With ABSD at 60% for foreigners, the traditional buyers for city-centre units had contracted sharply.

If this couple ever needed to sell, they would be competing for a smaller pool of eligible buyers.

We shared all of this openly.

Including the fact that steering them away from a $2 million condo would cut our commission roughly in half.

Most agents would have helped them buy the condo they came in asking for.

A young couple who wants to buy a specific $2M condo? A straightforward transaction in real estate.

But this couple was not optimising for capital gains or legacy planning at this stage.

They wanted space, comfort, and a home in a location they genuinely enjoyed.

When the full three-dimensional analysis showed that the condos matching that description:

👉 carried weak exit liquidity,

👉 Hidden maintenance costs,

👉 and a financing structure with almost no buffer,

the honest conclusion was not "buy a different condo."

It was "a condo is not the right first move."

So we sequenced it.

A five-room HDB resale in Boon Keng at $1.262 million.

A home that matched their lifestyle now while building the equity to make their eventual move into private property from a position of real strength.

Less than three years later, they are preparing to do exactly that.

Their unit is estimated at around $1.43 million, with a comparable unit on a higher floor selling for $1.55 million.

$168,000

Unrealised gains in less than three years

That is the foundation for their upgrade into private property down the line, one we will evaluate through the same 7-Point Institutional Property Scorecard, at the right price, on their terms.

Had they rushed into that original $2 million condo, they would not be choosing their next move.

They would be stuck in a property that was harder to sell, costlier to maintain, and offering none of the flexibility they have today.

Helping them buy that freehold they originally wanted would have earned us roughly double the commission.

But our analysis said that this specific freehold option was the wrong move for this family. That is all we needed to know.

CASE STUDY: THE ALTERNATIVE

Here is what it looks like when all three dimensions are part of the conversation.

A young couple came to us ready to upgrade. They had done their homework.

Budget of $2 million. They wanted a freehold condominium near the city.

Older boutique developments from the 1980s caught their eye.

Spacious layouts, central locations, the kind of units their parents might call "real property."

We understood the appeal.

And we could have collected a comfortable commission by helping them buy exactly what they wanted.

Instead, we asked them to let us run the full picture.

Not just "can I afford the monthly payment?" but whether the financing structure actually protects you.

Which loan package has costs buried in the fine print.

Whether your eligibility is calculated the way you think it is.

Whether there are options available to you that nobody has mentioned, because they require mortgage-level expertise to even know they exist.

Most buyers are never told about deviated rates that banks offer but do not publish.

Or about free conversion clauses within lock-in periods that can save thousands per year.

Or about the difference between a 0.75% and 1.5% cancellation penalty clause, and why it matters when you need to refinance.

These details sit in the second dimension. And they are almost always left out of the conversation.

DIMENSION 1: THE PROPERTY ✓

The older freehold condos had issues hiding behind the attractive price tags.

Ageing infrastructure that would need replacement within years.

One comparable development had recently charged residents $300 per month over two years just for lift upgrades.

Boon Keng HDB estate.

After factoring in $80,000 to $100,000 in realistic renovation costs, the "affordable" entry price was not affordable at all.

And when we checked transaction volume, the picture worsened.

Some of these boutique freehold developments had recorded just one or two transactions in an entire year.

When you can count the number of buyers on one hand, you are looking at a serious liquidity problem at exit.

DIMENSION 2: FINANCING ✓

Stretching to $2 million would have tightened their monthly cashflow significantly.

The financing stress-test showed limited buffer if interest rates moved even slightly.

DIMENSION 3: STRESS-TESTING ✓

CBD condos were facing a shrinking buyer pool.

With ABSD at 60% for foreigners, the traditional buyers for city-centre units had contracted sharply.

If this couple ever needed to sell, they would be competing for a smaller pool of eligible buyers.

We shared all of this openly.

Including the fact that steering them away from a $2 million condo would cut our commission roughly in half.

Most agents would have helped them buy the condo they came in asking for.

A young couple who wants to buy a specific $2M condo? A straightforward transaction in real estate.

But this couple was not optimising for capital gains or legacy planning at this stage.

They wanted space, comfort, and a home in a location they genuinely enjoyed.

When the full three-dimensional analysis showed that the condos matching that description:

👉 carried weak exit liquidity,

👉 Hidden maintenance costs,

👉 and a financing structure with almost no buffer,

the honest conclusion was not "buy a different condo."

It was "a condo is not the right first move at this stage."

So we sequenced it.

A five-room HDB resale in Boon Keng at $1.262 million.

A home that matched their lifestyle now while building the equity to make their eventual move into private property from a position of real strength.

Less than three years later, they are preparing to do exactly that.

Their unit is estimated at around $1.43 million, with a comparable unit on a higher floor selling for $1.55 million.

$168,000

Unrealised gains in less than three years

That is the foundation for their upgrade into private property down the line.

One we will evaluate through the same 7-Point Institutional Property Scorecard, at the right price, on their terms.

Had they rushed into that original $2 million condo, they would not be choosing their next move.

They would be stuck in a property that was harder to sell, costlier to maintain, and offering none of the flexibility they have today

Helping them buy that freehold they originally wanted would have earned us roughly double the commission.

But our analysis said that this specific freehold option was the wrong move for this family. That is all we needed to know.

The Invisible Factor That

Decided Both Outcomes

There is a pattern here.

And it shows up in nearly every property decision we have reviewed since entering real estate.

The family at One Pearl Bank did not buy a bad property.

The couple who came to us also had solid instincts.

In both cases, the first dimension was fine. The property analysis was reasonable.

But the factors that actually determined the outcome sat in the second and third dimensions.

Financing risk. Regulatory exposure. Exit liquidity.

Buyer pool dynamics. Total cost of ownership.

These are the things that turn a "good property" into a good outcome, or a painful one.

And they are almost never part of the standard property buying conversation.

Not because buyers are careless. But because the standard process is simply not designed to cover them.

Our banking backgrounds trained us to see this gap. In the institutions we came from, evaluating a deal on one dimension would not just be unusual.

It would be unacceptable.

We believe every family making a million-dollar property decision deserves that same standard of analysis.

We believe every family making a million-dollar property decision deserves that same standard of analysis.

The Invisible Factor That Decided Both Outcomes

There is a pattern here.

And it shows up in nearly every property decision we have reviewed since entering real estate.

The family at One Pearl Bank did not buy a bad property.

The couple who came to us also had solid instincts.

In both cases, the first dimension was fine. The property analysis was reasonable.

But the factors that actually determined the outcome sat in the second and third dimensions.

Financing risk. Regulatory exposure. Exit liquidity.

Buyer pool dynamics. Total cost of ownership.

These are the things that turn a "good property" into a good outcome, or a painful one.

And they are almost never part of the standard property buying conversation.

Not because buyers are careless. But because the standard process is simply not designed to cover them.

Our banking backgrounds trained us to see this gap. In the institutions we came from, evaluating a deal on one dimension would not just be unusual.

It would be unacceptable.

We believe every family making a million-dollar property decision deserves that same standard of analysis.

We believe every family making a million-dollar property decision deserves that same standard of analysis.

This is what we built our practice around.

Every client we work with goes through the same process we would apply to an institutional deal. Adapted for real families, with real constraints and real lives.

It starts with the second dimension.

Your actual financial position. Not the online calculator version.

The version that accounts for how banks really assess your eligibility.

What your debt servicing looks like under different rate scenarios.

And what financing options exist that most buyers are never told about.

Kalcee has secured loans for clients that other agents and brokers said could not be done.

Not through loopholes. Through understanding the system at a level that most people in property do not have access to.

The 7-Point Institutional Property Scorecard

Then we move to the first and third dimensions together.

We evaluate every property the way institutions evaluate deals. Every property goes through our 7-Point Institutional Property Scorecard.

Location, project fundamentals, supply dynamics, demand and liquidity, exit strategy, financial analysis, and risk stress-testing.

We look at who is realistically buying these units today, and whether that pool is growing or shrinking.

If a property does not pass the scorecard, we say so. Even if it means we lose the sale.

And we plan for the scenarios most people hope will never happen.

Interest rate shifts. Income disruption. Early exit. Cooling measure changes.

Not because we expect the worst.

But because a plan that only works under perfect conditions is not a plan.

We have walked clients away from purchases that would have earned us double the commission because the full analysis showed it was the wrong decision for that family.

We have shown buyers paths to homes they were told they could not afford.

We have helped families avoid six-figure mistakes they did not know they were about to make.

This is not something we offer on the side. It is the only way we work.

This is what we built our practice around.

This is what we built our practice around.

Every client we work with goes through the same process we would apply to an institutional deal. Adapted for real families, with real constraints and real lives.

It starts with the second dimension.

Your actual financial position. Not the online calculator version.

The version that accounts for how banks really assess your eligibility.

What your debt servicing looks like under different rate scenarios.

And what financing options exist that most buyers are never told about.

Kalcee has secured loans for clients that other agents and brokers said could not be done.

Not through loopholes. Through understanding the system at a level that most people in property do not have access to.

The 7-Point Institutional Property Scorecard

Then we move to the first and third dimensions together.

We evaluate every property the way institutions evaluate deals. Every property goes through our 7-Point Institutional Property Scorecard.

Location, project fundamentals, supply dynamics, demand and liquidity, exit strategy, financial analysis, and risk stress-testing.

We look at who is realistically buying these units today, and whether that pool is growing or shrinking.

If a property does not pass the scorecard, we say so. Even if it means we lose the sale.

And we plan for the scenarios most people hope will never happen.

Interest rate shifts. Income disruption. Early exit. Cooling measure changes.

Not because we expect the worst.

But because a plan that only works under perfect conditions is not a plan.

We have walked clients away from purchases that would have earned us double the commission because the full analysis showed it was the wrong decision for that family.

We have shown buyers paths to homes they were told they could not afford.

We have helped families avoid six-figure mistakes they did not know they were about to make.

This is not something we offer on the side. It is the only way we work.

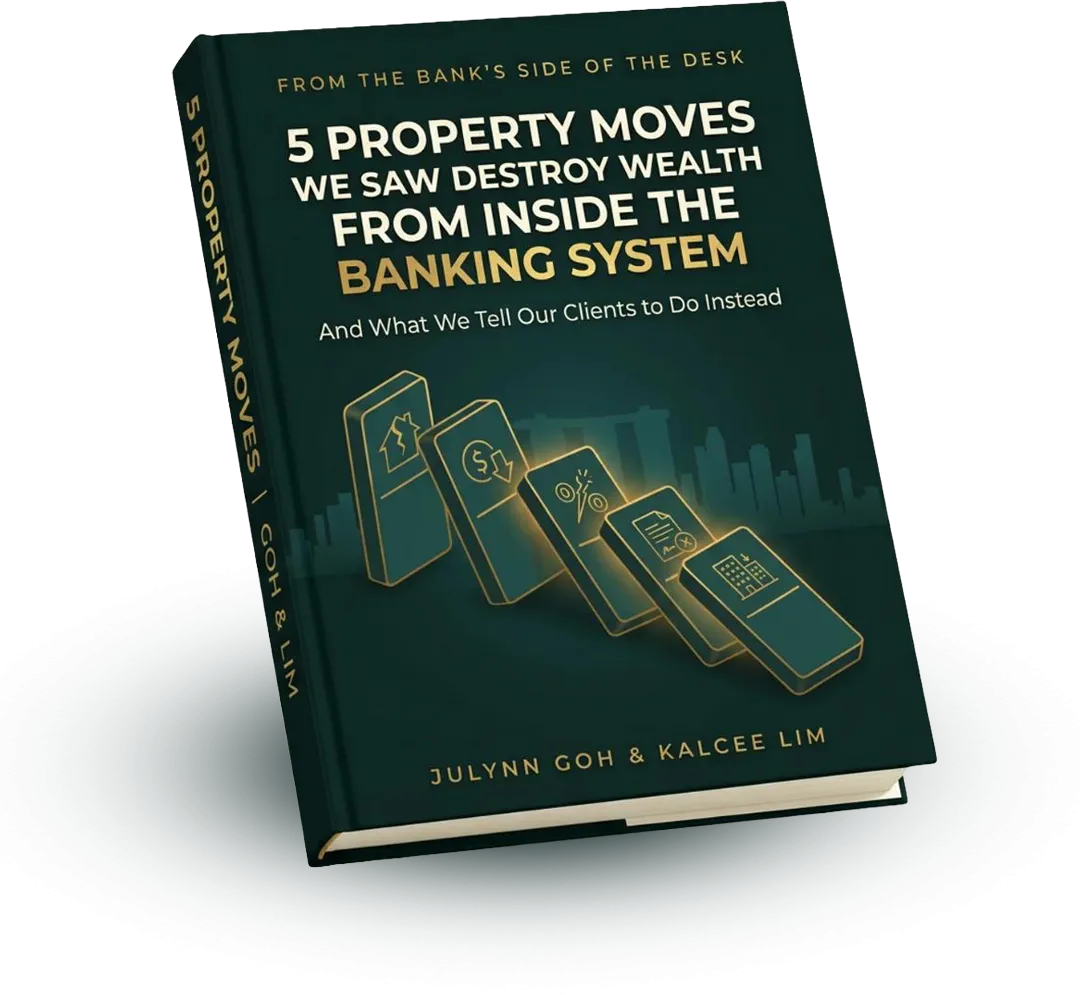

5 Property Moves We Saw Destroy Wealth From Inside the Banking System

(And What We Tell Our Clients to Do Instead)

We took the five property decisions where we have seen the biggest gap between what buyers expect and what actually happens.

And broke each one down across all three dimensions.

Each section draws from real transaction data, named developments, and cases we have worked on directly.

Inside, you will find:

⚠️ Why the property that sold 90% of units on launch day underperformed the one that sold less than 30%. And what this reveals about how most buyers misjudge demand.

⚠️ Why saving $26,000 in interest by waiting for rates to drop cost one buyer $110,000 in purchase price. And the question you should ask instead of "when will rates come down?"

⚠️ Why "freehold" does not protect you the way most buyers assume. And the metric that actually predicts whether you can exit when you need to.

⚠️ A financing blind spot that costs buyers $15,000 to $30,000 that almost no one catches. Because it sits in the second dimension that most property conversations never reach.

⚠️ Why a property that checks every box can still lose you money. And the single factor that separates a sound purchase from one that only looks like it.

More importantly, each section includes what we recommend instead.

Not generic advice. The same thinking we apply with every client we take on.

5 Property Moves We Saw Destroy Wealth From Inside the Banking System

(And What We Tell Our Clients to Do Instead)

We took the five property decisions where we have seen the biggest gap between what buyers expect and what actually happens.

And broke each one down across all three dimensions.

Each section draws from real transaction data, named developments, and cases we have worked on directly.

Inside, you will find:

⚠️ Why the property that sold 90% of units on launch day underperformed the one that sold less than 30%. And what this reveals about how most buyers misjudge demand.

⚠️ Why saving $26,000 in interest by waiting for rates to drop cost one buyer $110,000 in purchase price. And the question you should ask instead of "when will rates come down?"

⚠️ Why "freehold" does not protect you the way most buyers assume. And the metric that actually predicts whether you can exit when you need to.

⚠️ A financing blind spot that costs buyers $15,000 to $30,000 that almost no one catches. Because it sits in the second dimension that most property conversations never reach.

⚠️ Why a property that checks every box can still lose you money. And the single factor that separates a sound purchase from one that only looks like it.

More importantly, each section includes what we recommend instead.

Not generic advice. The same thinking we apply with every client we take on.

BEFORE YOU DOWNLOAD

Is This Guide Right for You?

This guide is for you if:

You’re a current home owner or first time buyer and you are seriously thinking about upgrading to a condo or EC within the next 12 months.

Maybe you have been watching property videos on YouTube, reading articles, or following what your friends who recently upgraded are doing.

Maybe you have started browsing PropertyGuru, visited a showflat or two, or even spoken to an agent.

But something still does not feel settled.

You are not sure if now is the right time, whether the finances actually work, or how to tell a genuinely sound purchase from one that just looks good on the surface.

You want to get this right.

You are open to being told that what you are considering might not be the best move, if the analysis supports it.

And you would rather slow down and make a sound decision than rush into one you regret.

This guide is not for you if:

You are looking for a list of "hot picks" or properties to flip for quick profit.

That is not how we think and it is not what this guide covers.

You want an agent who will tell you what you want to hear.

We will tell you what the analysis shows, even when it is not what you were hoping for.

You have already made your decision and just want someone to say yes.

This guide is for people who are still thinking, not people who have already committed.

BEFORE YOU DOWNLOAD

Is This Guide

Right for You?

This guide is for you if:

You’re a current home owner or first time buyer and you are seriously thinking about upgrading to a condo or EC within the next 12 months.

Maybe you have been watching property videos on YouTube, reading articles, or following what your friends who recently upgraded are doing.

Maybe you have started browsing PropertyGuru, visited a showflat or two, or even spoken to an agent.

But something still does not feel settled.

You are not sure if now is the right time, whether the finances actually work, or how to tell a genuinely sound purchase from one that just looks good on the surface.

You want to get this right.

You are open to being told that what you are considering might not be the best move, if the analysis supports it.

And you would rather slow down and make a sound decision than rush into one you regret.

This guide is not for you if:

You are looking for a list of "hot picks" or properties to flip for quick profit.

That is not how we think and it is not what this guide covers.

You want an agent who will tell you what you want to hear.

We will tell you what the analysis shows, even when it is not what you were hoping for.

You have already made your decision and just want someone to say yes.

This guide is for people who are still thinking, not people who have already committed.

Your Property Decision Will Shape Your Family's Financial Life for the Next 10 to 15 Years.

Don't make it based on one dimension of analysis when the outcome depends on three.

P.S. — We know property decisions are personal. Every family's finances, timeline, and priorities are different. The guide covers the patterns we see most often, but it cannot account for your specific situation.

If after reading it you want to talk through how any of this applies to you, we are happy to sit down and go through it together.

That is how every client relationship we have starts.

A conversation, not a pitch.

Your Property Decision Will Shape Your Family's Financial Life for the Next 10 to 15 Years.

Don't make it based on one dimension of analysis when the outcome depends on three.

P.S. — We know property decisions are personal. Every family's finances, timeline, and priorities are different. The guide covers the patterns we see most often, but it cannot account for your specific situation.

If after reading it you want to talk through how any of this applies to you, we are happy to sit down and go through it together.

That is how every client relationship we have starts.

A conversation, not a pitch.

Copyright 2026. All rights reserved.

Copyright 2026. All rights reserved.